Our Bitcoin price forecasting paper under consideration for journal Best Paper Award

Our paper titled Next-Day Bitcoin Price Forecast published on June 2019 in the Journal of Risk and Financial Management is under consideration for the journal Best Paper Award 2020.

Below are the highlights of the paper:

- Comparison between ARIMA and ANN models in bitcoin price forecasting.

- We show that model re-estimation using extending window for next-day bitcoin price forecast does not improve forecast performance.

- A sensitivity analysis on the impact of lag length on the forecast performance for ANN models shows that increasing lag length not necessarily improves forecast performance of ANN models.

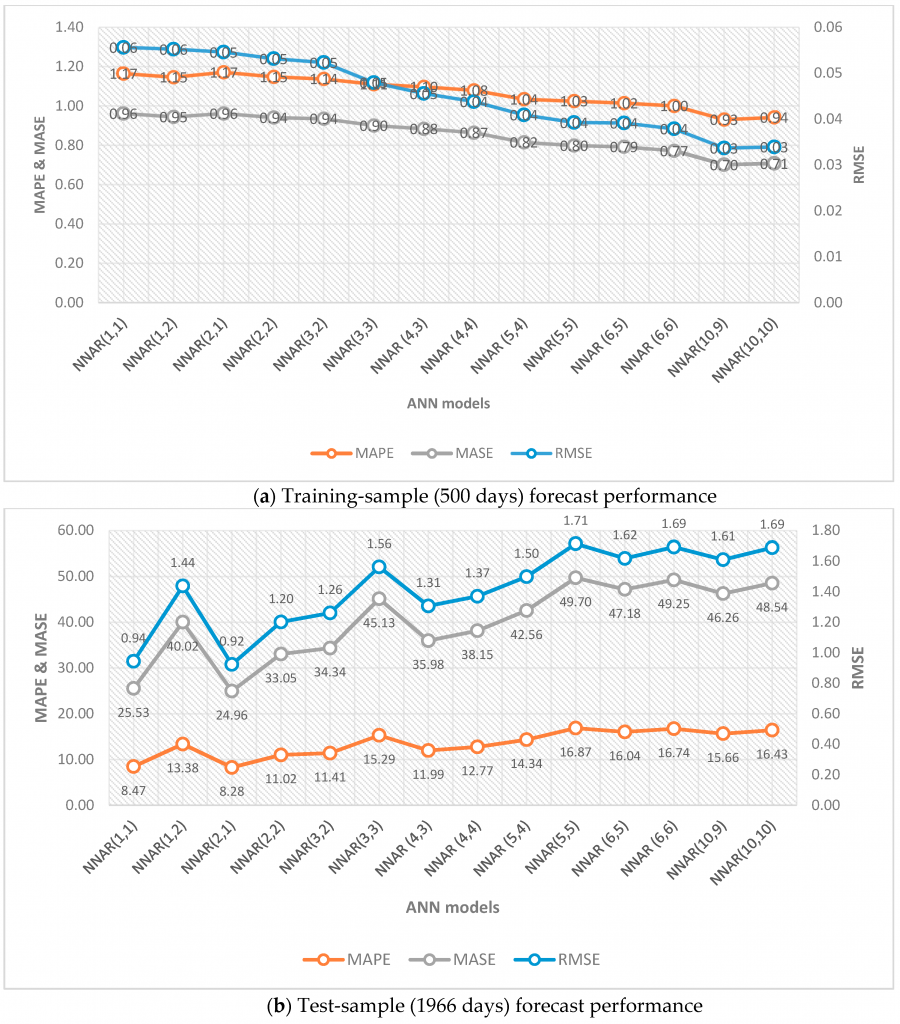

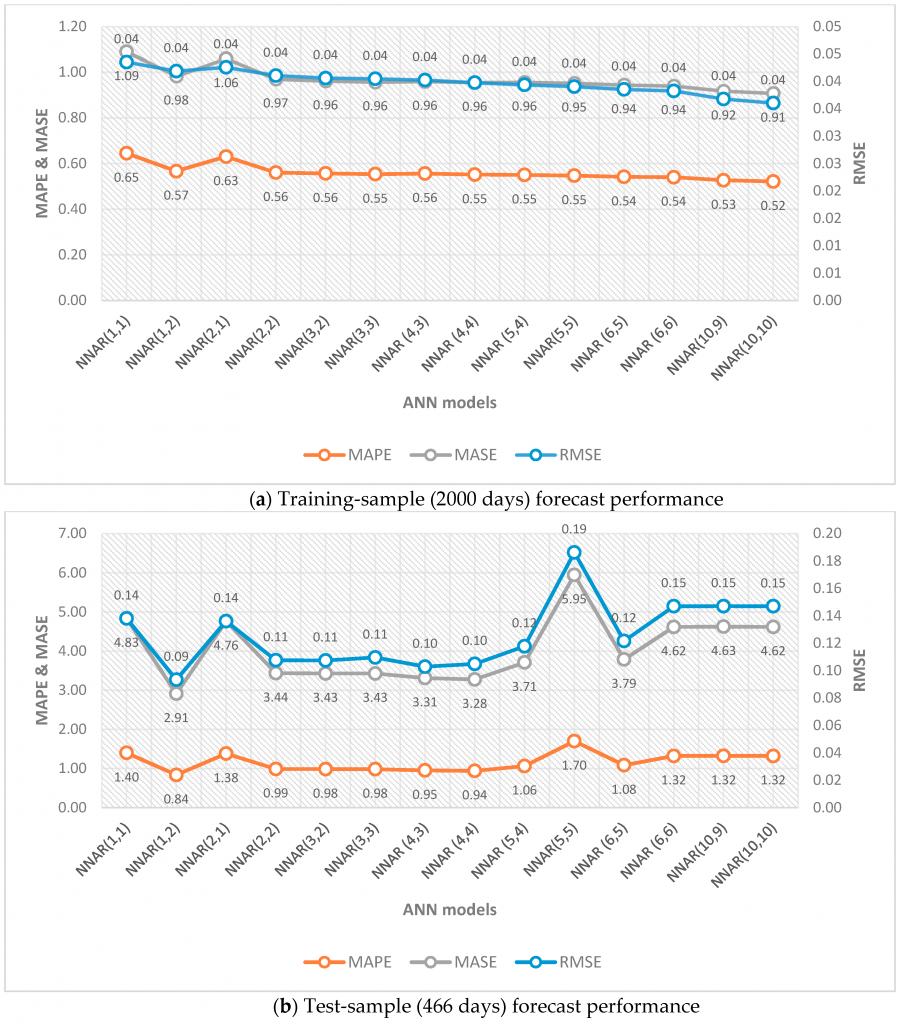

- Size of training sample has an effect on ANN model’s optimal lag length. While training data using smaller training sample (500 data points), increasing lag length seems to improve forecast performance, but a larger training sample (2000 data points) diminishes this impact. See the following figures.

To read the full paper from journal website, click here!