Seminar presentation at NHH

I was invited by the Head of the Department of Business and Management Science of the NHH Norwegian School of Economics for a seminar presentation on August 30, 2019.

I presented a working paper titled ” Container freight forecasting with and without model re-estimation in expanding horizon”. Below I present the highlight and a brief summary of the study.

Highlights

- Container freight rate entails seasonal component.

- CCFI is nonlinear and its dynamics is well explained by nonlinear space state model.

- Model re-estimation at next-step forecast does not improve forecast performance.

- Combination of linear (i.e. SARIMA) and nonlinear (i.e. TBATS) models provide best forecast outcome.

- For individual models, TBATS shows great potential, particularly for forecasting multiple-step ahead.

Summary

Short-term forecast of container freight is essential for major maritime players including ship owners, shipping lines, shippers and even for the port authorities. This study compares three univariate models — ARIMA, Neural Network Autoregression (NNAR) and TBATS, and finds that TBATS or combination of TBATS and ARIMA forecast, outperforms ARIMA and NNAR both in training and test-sample forecast. To the best of author’s knowledge, an application of TBATS is not evident in forecasting container freight. Moreover, this study adopted the model re-estimation technique for the next-step expanding forecast for test-sample in addition to the conventional approach to forecast test-sample using a selected model based on the training-sample. As a proxy for weekly container freight, China Container Freight Index (CCFI) is forecasted, collected from the Shanghai Shipping Exchange from January 2010 to December 2018, in total 470 data points. For cross-validation, two expanding training-samples, one from January 2010 till December 2016 and another from January 2010 till December 2017 are analysed. Subsequently, two test-samples, January-December 2017 and January-December 2018 are forecasted.

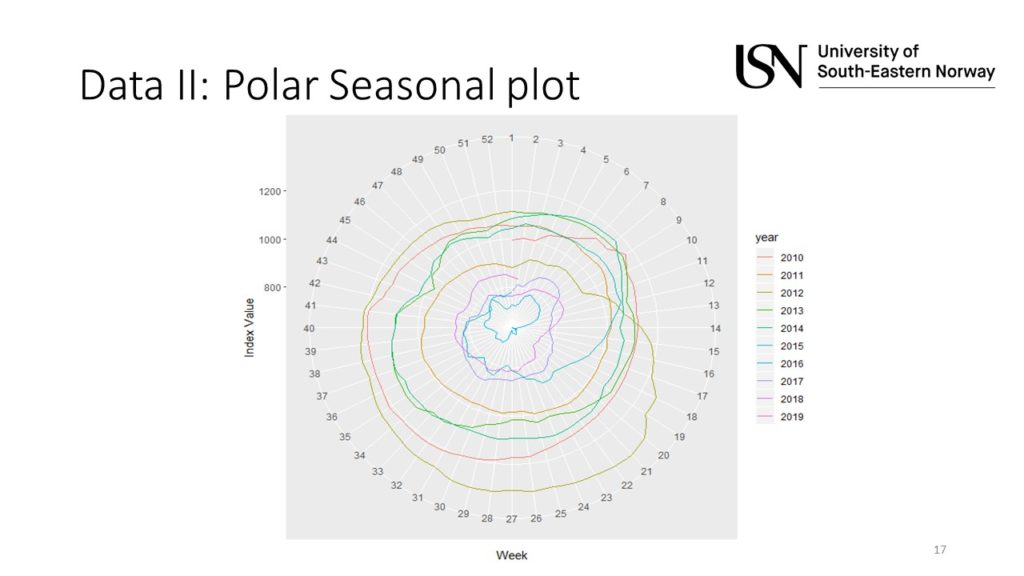

The above picture is a snapshot of the analysis of seasonality in CCFI using seasonal polar plot. As soon as the study will be published in a journal, I will update the full paper link here!